Table of Contents

Are you looking to file bankruptcy but not sure where to start?

This guide will tell you everything you need to know before you start your bankruptcy. We will guide you through every step of the process from when you should start to what it costs all the to preparing you to file.

Don't have time to read the entire guide now?

Fill out the form for a downloadable PDF version of the guide you can reference later.

Chapter 1 Understanding Chapter 13 Bankruptcy in Arizona

The desert sun cast long shadows across the vast expanse of Arizona as Sarah sat in her modest home, surrounded by stacks of unpaid bills and looming financial uncertainty. The weight of debt had become an unyielding burden, pressing down on her with each passing day. It was then that she began to consider Chapter 13 bankruptcy—a lifeline that promised a chance to regain control of her financial future.

The Journey Begins

Chapter 13 bankruptcy stands as a beacon of hope for individuals like Sarah, offering a structured pathway to reorganize and repay debts while retaining valuable assets. But what exactly is Chapter 13 bankruptcy, and how does it differ from other forms of bankruptcy?

At its core, Chapter 13 is a powerful tool within the legal framework that allows individuals with a steady income to develop a repayment plan, consolidating debts and making manageable payments over a specified period, typically three to five years. Unlike Chapter 7 bankruptcy, which involves liquidating assets to discharge debts, Chapter 13 focuses on restructuring and repayment.

The Essence of Chapter 13 Bankruptcy

In Arizona, Chapter 13 bankruptcy provides a structured means for individuals to address their financial obligations while maintaining ownership of their property. It’s often seen as a constructive solution for those who don’t qualify for Chapter 7 or wish to protect valuable assets from liquidation.

The cornerstone of Chapter 13 bankruptcy lies in the creation of a repayment plan crafted in collaboration with a court-appointed trustee. This plan outlines how debts will be repaid over the designated period, ensuring affordability and feasibility for the filer. The duration of the plan depends on various factors, including income, expenses, and the total amount of debt owed.

Protection and Preservation

One of the primary advantages of Chapter 13 bankruptcy is its ability to shield assets from liquidation. In Arizona, individuals can retain ownership of their homes, vehicles, and other essential possessions while adhering to the agreed-upon repayment plan. This protection provides a sense of security, allowing filers to retain crucial assets vital for their livelihood.

The Qualification Criteria

Not everyone is eligible for Chapter 13 bankruptcy. To qualify in Arizona, individuals must have a regular income source that enables them to make monthly payments outlined in the repayment plan. Additionally, there are limits to the amount of secured and unsecured debt allowable for Chapter 13 eligibility.

The Filing Process

Embarking on a Chapter 13 bankruptcy journey in Arizona initiates with filing a petition in the bankruptcy court. Alongside the petition, filers must submit a comprehensive overview of their financial situation, including income, expenses, assets, and liabilities. This detailed disclosure forms the foundation upon which the repayment plan will be constructed.

Upon filing, an automatic stay is issued, halting creditor actions such as foreclosure, repossession, or wage garnishment. This legal injunction provides a breathing space for individuals to regroup and proceed with the bankruptcy proceedings.

The Trustee’s Role

A pivotal figure in the Chapter 13 bankruptcy process is the trustee appointed by the court. The trustee’s responsibilities encompass reviewing the proposed repayment plan, ensuring its compliance with bankruptcy laws, and overseeing the distribution of payments to creditors. Their guidance and oversight are integral to the successful execution of the repayment plan.

Conclusion

Chapter 13 bankruptcy in Arizona isn’t merely a legal process; it’s a journey toward financial stability and a fresh start. For individuals burdened by overwhelming debt, it offers a structured pathway to regain control and work toward a brighter financial future. Understanding the nuances and procedures of Chapter 13 is the first step towards navigating this transformative process.

Chapter 2 What Happens When You File Chapter 13 Bankruptcy in Arizona?

People who are preparing to file for Chapter 13 bankruptcy need to know that it can take some time to get the results they are seeking. While a Chapter 7 case only takes six or fewer months, a person will usually commit to paying a Chapter 13 repayment plan for three to five years.

Considerable work needs to be performed before a person can even file for Chapter 13 and they then have to endure repayment plan approval and confirmation hearings. When a person is able to present a repayment plan they know they can stick to and complete without any issue, they can usually achieve a discharge that frees them from authorized debts.

Preparing to File for Chapter 13

Only individuals can file for Chapter 13, not businesses, and there cannot be a prior bankruptcy petition dismissal within the past 180 days. A person cannot have more than $465,275 in unsecured debts or $1,395,875 in secured debts, they must be current on their income taxes and have sufficient income to pay their debts.

All people who are filing for bankruptcy in Arizona must complete credit counseling from a United States Trustee-approved credit counseling agency and receive a credit counseling certificate. When a person fails to complete credit counseling before filing a petition or not meeting the requirements of an extension to complete counseling after filing, a case can be dismissed without refund of any filing fee paid, there will be no discharge of debts, and any refiling a year after dismissal means automatic stay protection will be limited to 30 days.

A bankruptcy court will only allow a person to complete a course after filing when they satisfy all of the necessary conditions, which include:

- They tried to get credit counseling from an approved agency before bankruptcy but were not able to obtain the counseling during the 7-day period after they made the request;

- Exigent (emergency) circumstances existed that made it necessary for them to file their case immediately; and

- They filed a certification stating the facts regarding the first two conditions with their petition.

The United States Department of Justice has a list of approved providers of personal financial management instructional courses. There are also certain things people should avoid doing after filing for Chapter 13.

Avoid going on shopping trips involving debt there is no intention to repay. Also avoid concealing any assets, as attempts to hide possessions can lead to seizure of assets and criminal charges.

Filing for Chapter 13

People filing for Chapter 13 bankruptcy create their own repayment plans, and the plans must be written and submitted to the bankruptcy court. Bankruptcy courts provide forms for creating plans, or people can obtain them from lower courts.

A bankruptcy court must approve a repayment plan for a person to enter into Chapter 13. A repayment plan will detail a person’s income, property, expenses, and debts with a proposed payment plan.

The Chapter 13 trustee reviews the plan, assesses its compliance with bankruptcy laws, collects payments, distributes payments to creditors, and ensures all terms of a bankruptcy repayment plan are followed. A repayment plan is usually divided into three categories:

- Priority Debts — Domestic support obligations, tax debts, and certain other debts may require 100 percent repayment as soon as possible.

- Secured Debts — Mortgage and car loan payments are two common kinds of secured debts for which people have property connected to the debts, and these also need to be repaid in full.

- Unsecured Debts — An unsecured debt has no collateral and includes credit card debt, utility bills, and personal loans. People may repay all of these debts or only a fraction, possibly even none of this debt.

Chapter 13 Meetings

When a person files for Chapter 13, they often have to begin making payments to their trustee even when their repayment plan has not yet been approved. It is usually within two months that a trustee will hold a meeting of the creditors, at which the trustee and the creditors can both ask questions of the debtor.

A debtor must attend this meeting to answer questions about their finances and proposed repayment plan. The next meeting after a meeting of the creditors will be a confirmation hearing, usually within 45 days.

The confirmation hearing decides whether a repayment plan will be acceptable and satisfies the terms of the Bankruptcy Code. A trustee begins distributing funds to creditors when a plan is approved, but failure to confirm a plan can lead to a person trying to convert their case to a Chapter 7.

The Chapter 13 Discharge

A person will be entitled to a discharge of all debts provided for by a repayment plan or disallowed when they complete all payments under their repayment plan. This means that a person can seek a discharge once they complete their repayment plan.

Debts that are not discharged under bankruptcy will usually include the priority debts and secured debts. It can take three to five years to reach the discharge, depending on the length of your repayment plan.

Chapter 3 How Much Does It Cost To File Chapter 13 in Arizona?

Many people who are in the midst of considering filing for bankruptcy are doing so because they do not have much money, so it can be hard for the same people to accept that it costs money to file for bankruptcy. Any bankruptcy case involves the basic filing fee for a petition as well as numerous other fees for other court motions or court services.

In Chapter 13 bankruptcy cases, people are generally not allowed to get filing fees waived or pay them in installments. Because Chapter 13 intends to keep a person current with payments, a filing fee being unaffordable can cause a court to question a person’s ability to succeed in a Chapter 13 case.

Credit Counseling Fee Waivers

A person who files for Chapter 13 must take two educational courses before they can receive a bankruptcy discharge wiping out qualifying debt. The United States Department of Justice Trustee Program website has a list of approved credit counseling agencies.

After completing credit counseling, a person still needs to take debtor education coursework. Certificates of completion for both classes will be required.

Credit counseling course costs often vary by provider, and many courses are about $50. If you register with a credit counseling agency, you will likely be asked if you want a fee waiver, and you should answer yes to this question.

There may be a requirement to submit a formal application, proof of income, and a completed budget worksheet. A majority of the questions on an application relate to income and family size.

It usually takes around 72 hours for a response as to whether a person qualifies for a fee waiver. When the fee is waived, a person can take the class for free, but people who are not approved must reapply.

Bankruptcy Filing Fee Waivers

There is a $313 filing fee for a Chapter 13 petition. Fees cannot be waived in Chapter 13 cases.

You may be able to file an Official Form 103A, Application for Individuals to Pay the Filing Fee in Installments. The number of installments will be limited to four, and a person must make the final installment payment no later than 120 days after filing their petition.

A person must file a repayment plan with their petition or within 14 days after their petition is filed, and a plan must be submitted for court approval and provide for payments of fixed amounts to the trustee on a regular basis, usually biweekly or monthly.

A trustee distributes funds to creditors according to the terms of the plan. A debtor must begin making payments to a trustee within 30 days of filing a bankruptcy case, even if the plan is not yet approved by the court.

Many debtors agree to make plan payments through payroll deductions because such agreements usually guarantee payments will be made on time and debtors will complete their plans. A person becomes eligible for discharge upon completion of all of their payments under a plan.

Hiring a Lawyer for Your Chapter 13 Bankruptcy Case

Many people want to try and file for bankruptcy on their own without hiring an attorney, and this often proves to be a mistake. It is not until people are in court that they realize how much help they need, and irreparable damage to bankruptcy cases forces people to reverse course.

A lawyer handling Chapter 13 bankruptcy cases will charge more than a Chapter 7 attorney because there will be much more work to do in a Chapter 13 case. A bankruptcy lawyer will know which chapter you should file for, advise you on how the process will work, and determine the debts that can be discharged in your case.

The attorney also serves a valuable role by advocating for a person’s interests during the meeting of the creditors. While people can hire Chapter 7 bankruptcy attorneys for less than $1,000, a Chapter 13 lawyer will usually cost several thousands of dollars with $3,000 being the national average.

A lawyer is going to be able to help you by preparing all of the necessary paperwork for your case, multiple forms that can be incredibly confusing for the average person to fill out by themselves. The attorney can also represent a person at all hearings they need to attend, and it can be invaluable for most people to have legal representation in these circumstances.

Chapter 4 How Long Does It Take To File Chapter 13 Bankruptcy in Arizona?

When a person files for Chapter 13 bankruptcy, they are entering a repayment plan that lasts three to five years, so there is not much hope in terms of wrapping up a bankruptcy case quickly when you are dealing with Chapter 13. In addition to the time you actually spend completing paperwork and attending required hearings, you are going to need to invest significant time in preparing to file.

Filing for Chapter 13 will require you to get all of your debts together so you can be sure that your discharge ultimately applies to all of your debts. It can take time to earn approval for a repayment plan, but you will want to be working toward beginning your payments and resolving your case.

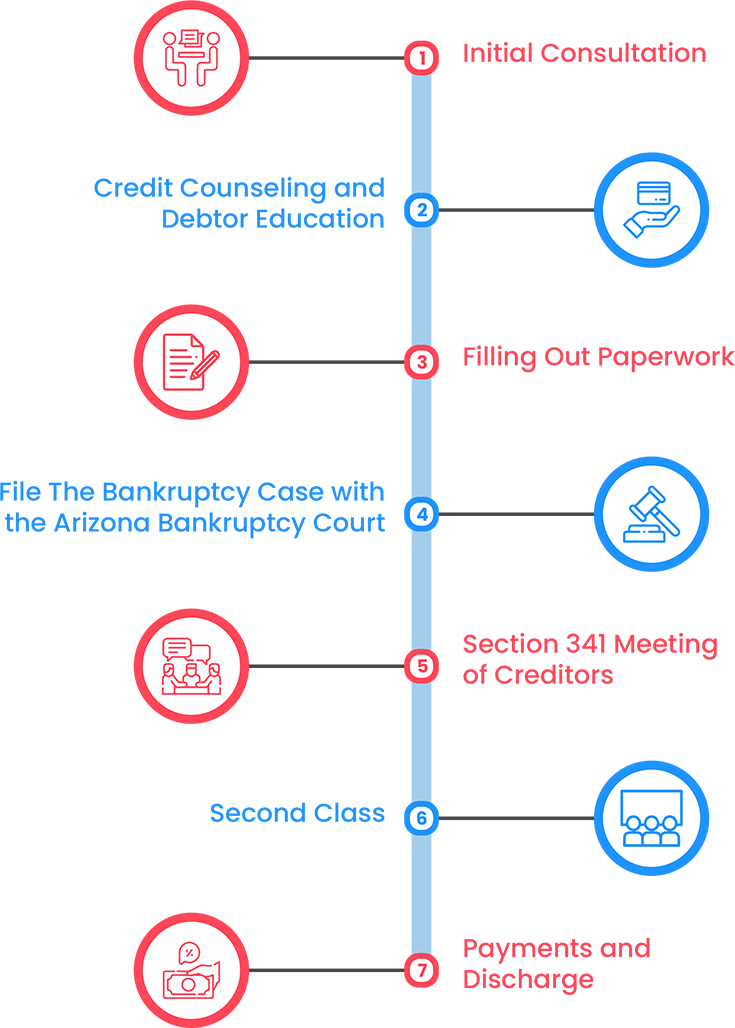

The Chapter 13 timeline

A Chapter 13 bankruptcy case usually unfolds as follows:

- Initial Consultation — A person should always take the time to contact an experienced Arizona bankruptcy attorney to evaluate their options. Not all people benefit from Chapter 13, especially when they are able to file for Chapter 7. When you speak to a lawyer about your case, they will tell you which documents they will need from you to proceed with your case and also advise you about how you will spend in the coming days.

- Credit Counseling and Debtor Education — Before a person can file for bankruptcy, they must complete pre-bankruptcy credit counseling and pre-discharge debtor education. Certificates of completion for both credit counseling and debtor education will be necessary before a filer’s debts can be discharged, but only credit counseling organizations and debtor education course providers approved by the United States Trustee Program can issue certificates. A credit counseling and pre-discharge debtor education course could break into two classes, and you need to attend both on time because failure to attend can lead to dismissal of your petition.

- Filling Out Paperwork — A person must fill out bankruptcy schedules and statements required for the Arizona Bankruptcy Court to look into their current financial status. They must provide information relating to their assets, debts, current income, and monthly expenses, as well as a summary of financial transactions before they file their case. When a person hires a bankruptcy lawyer, the attorney can usually handle all of the paperwork for them. A person may need to fill out a questionnaire that provides the law firm with the information to complete the schedules and statements.

- File The Bankruptcy Case with the Arizona Bankruptcy Court — When a person files a Chapter 13 bankruptcy case, there is a $313 filing fee for a new petition and a $25 filing fee to convert a Chapter 13 case to a Chapter 7 case. A person filing Chapter 13 will be given a case number they can then give to their creditors, although filing Chapter 13 should immediately create the automatic stay that prohibits creditors from taking any further collection actions.

- Section 341 Meeting of Creditors — The Meeting of Creditors occurs between 30 to 45 days after a petition is filed, and a person filing for Chapter 13 needs to attend the hearing. An attorney may represent people but cannot appear on their behalf. While “meeting of the creditors” creates a lot of fear in people, several creditors will not even bother to attend. There is a series of 10 to 15 questions from a trustee about a case, but none of the questions will be anything that catches a person off guard.

- Second Class — A second credit counseling and pre-discharge debtor education class is often scheduled for within 60 days of the Section 341 meeting. Attending this class is again mandatory.

- Payments and Discharge — Chapter 13 again requires a person to enter a repayment plan for three to five years, and all payments need to be made on time. After a person completes every payment required under their plan and honors any requests of a trustee, then can be eligible for a discharge. It often takes courts a little longer than this to process paperwork.

For many people filing Chapter 13 bankruptcy, there is a primary concern with saving a home or car that people are still making payments on. The good news for these filers is that payments on secured debts such as houses and motor vehicles can be worked into repayment plans.

After a person files for Chapter 13 bankruptcy, they will want to begin following up on their own credit reports. Creditors do not have to report payments made during a Chapter 13 repayment plan, but you should make sure that all creditor balances are zero within four months of a Chapter 13 discharge.

Rebuilding your credit after filing for Chapter 13 can take some time, but there are things you can do that will help you in the long run. Avoid working with any credit repair companies but consider credit-builder loans or secured credit cards. Make sure that you spend responsibly and can pay your bills at the end of each month.

Chapter 5 How Often Can You File Chapter 13 Bankruptcy in Arizona?

While many people want to think of bankruptcy filings as being truly once-in-a-lifetime awful events, the truth is that there are several people who can find themselves in situations in which they must file for bankruptcy again after already having filed once before. People need to understand that there is no limit on the number of times a person can file for bankruptcy, so any person who might have a second or subsequent bankruptcy filing will want to work with an Arizona bankruptcy attorney.

Second or subsequent bankruptcy cases can be more complicated in some areas, however. After a court forgives debt, people typically need to wait a period of years before they can seek to have more debt forgiven.

Chapter 13 Filing Timelines

Two years to file Chapter 13 after Chapter 13

Four years to file Chapter 13 after Chapter 7

Six years to file Chapter 7 after Chapter 13

Eight years to file Chapter 7 after Chapter 7

The good news for people filing Chapter 13 bankruptcy cases is that the wait times are actually the shortest between Chapter 13 cases. When you previously filed a Chapter 7 case, there could be a longer wait time.

The wait times usually break down as follows, with Chapter 13 cases usually involving the shortest waits:

- Two Years to File Chapter 13 After Chapter 13 — The typical Chapter 13 plan takes three to five years to complete, so it is not terribly common for people who just completed those plans to re-enter new ones. Some people may be seeking new repayment plans after previous ones failed because of extreme hardship. Filing for Chapter 13 before a two-year wait period is up can lead to a denial of a second discharge and a debtor remaining liable for all debts not paid through the prior Chapter 13 plan.

- Four Years to File Chapter 13 After Chapter 7 — Some people can work around the four-year restriction by “double filing” or “filing Chapter 20,” which means 13+7. People may argue they need to file Chapter 13 to deal with debts their Chapter 7 filing could not discharge. Filing for Chapter 13 before a four-year wait period is up can lead to a denial of a second discharge and a debtor remaining liable for all their debts. Filing Chapter 20 can allow people to wipe out more debts over time and catch up on past-due debts, but there will be a greater requirement to prove a person is acting in good faith.

- Six Years to File Chapter 7 After Chapter 13 — People seeking Chapter 7 protection after filing Chapter 13 have to wait six years but could be able to waive the wait period if they pay their unsecured debts in full in their original Chapter 13 case or paid at least 70 percent of their plan in good faith and made their best effort to repay.

- Eight Years to File Chapter 7 After Chapter 7 — Although Chapter 7 is usually considered the quickest possible bankruptcy case, it also has the longest wait of any time between cases. Filing again before the eight-year wait period is up will lead to a denial of a second discharge and a debtor remaining liable for all their debts.

Many people have concerns about having never received a discharge on the bankruptcy chapter they originally filed under. If a court dismisses a bankruptcy case, a person will usually be able to file again in 180 days.

People can often file again unless they did not obey a court order or their case was voluntarily dismissed because of a creditor filing a motion to lift an automatic stay. If a person is filing for Chapter 13 a second time after their first attempt was denied, then the clear issue will probably be an inability to get the court to honor many of the same debts listed on the first attempt.

Filing repeat bankruptcies can reduce automatic stay protections in some cases, so you want to consult a lawyer about how much protection you actually have. You may also need to prepare for the possibility that filing multiple bankruptcies could be seen by a court as being abusive.

If a person files for Chapter 13 after receiving a Chapter 7 discharge, they can also catch up on debts they incurred after filing the first time. People filing for Chapter 13 twice may be able to extend their repayment plans.

Some people need to be careful, however, so they do not find themselves ineligible for a discharge or not getting adequate protection from creditors. If a judge finds they are filing cases in bad faith, it can prevent them from filing any more.

It is important to remember that Chapter 13 does less damage to your credit report than Chapter 7. Whereas Chapter 7 stays on your credit record for a decade, Chapter 13 only lasts seven years.

Chapter 6 What Debts Can Be Discharged in a Chapter 13 Bankruptcy in Arizona?

Chapter 13 bankruptcy has an inherent edge over Chapter 7 in that certain debts can be discharged in a Chapter 13 case that cannot be in a Chapter 7 case. Discharging debts in Chapter 13 will be far more difficult because a person first needs to complete a three- to five-year repayment plan whereas a person filing Chapter 7 only needs to file and get their debts discharged.

A person filing Chapter 13 must pay the greater of their disposable income or the value of their nonexempt property. A person filing Chapter 13 may be able to pay less than they owe, but others will have to pay it all to close their cases.

Debts Commonly Discharged in Chapter 13

When a person files Chapter 13, there are three types of debt claims: priority, secured, and unsecured. Priority claims are granted special status, such as taxes and costs of bankruptcy proceedings.

Secured claims involve creditors having the right to take back property if a debtor does not pay the underlying debt. Unsecured claims involve creditors having no special rights to collect against particular property owned by a debtor.

The most common kinds of unsecured debt discharged in Chapter 13 cases include, but are not limited to:

- credit card debt

- medical bills

- phone bills

- personal loans from friends, family, and employers

- past-due rent or other money owed under lease agreements

- business debts

- collection agency accounts

- auto accident claims

- unpaid utility bills

- repossession or foreclosure deficiency balances

- civil court judgments

- judgments from unpaid credit card debt, medical bills, or other unsecured debt

- old tax penalties and unpaid taxes

- attorneys’ fees

Other debts that can be discharged in Chapter 13 but not Chapter 7 include willful and malicious damage to another person’s property, debts incurred to pay nondischargeable tax obligations, and child support, alimony, spousal maintenance, or spousal support obligations could be reduced through Chapter 13 repayment plans in some cases. A Chapter 13 case can also get rid of homeowners’ dues when a person surrenders their home and government fines, penalties, or liens.

While you want to understand what debts can be discharged in Chapter 13, it is also important to understand the debts that cannot be discharged in Chapter 13. Federal and private student loans are a good example of a debt that is not dischargeable in bankruptcy unless a person can prove that their loan payment imposes an “undue hardship” on them, their family, and their dependents.

When a person has secured debts, they can either pay as they agreed or surrender their collateral, and surrendering the collateral will mean the debt becomes a nonpriority unsecured debt. When a person is behind on a long-term debt, they can make up payments through their repayment plan.

A person cannot discharge any debt that was incurred under false pretenses, which means things people buy without intention to pay for it. Debt incurred under false pretenses is extremely common in many bankruptcy cases because people assume they can max out the credit cards before filing, but this is always a mistake because courts frequently uncover the expenses and hold people accountable.

You should also remember how many luxury purchases you made before you decide to file for bankruptcy because debts people incur within 90 days of their bankruptcy filings for luxury goods or services worth $800 or more owed to a single creditor are nondischargeable. This is also true for cash advances of $1,100 or more taken within 70 days of a bankruptcy filing.

Unpaid taxes, such as tax liens, can also survive a bankruptcy discharge, although taxes that are several years old could be discharged. A tax lien remains attached to your property, so you will still be responsible for that after Chapter 13.

Property taxes people incur before filing for Chapter 13 are also nondischargeable. Property taxes payable more than one year before filing could be discharged, however.

You also cannot discharge employment taxes, trust fund taxes, or nondischargeable taxes. You could also remain responsible for condominium dues and fees, pension plans, and personal injury or wrongful death damages from drunk driving cases.

When people are not satisfied with the types of debt that Chapter 13 can wipe out, then it may be advisable for them to seek the help of a debt relief organization. You need to exercise extreme caution in working with any debt relief company because there are several frauds and scam artists seeking to take advantage of people.

It may be possible for you to work with a reputable debt relief company that helps you negotiate more flexible repayment terms with your creditors and help you find some financial relief that you are seeking. You could also benefit from speaking to a financial advisor in some cases.

Chapter 7 What Are The Advantages Of Filing Chapter 13 Bankruptcy in Arizona?

People who are preparing to file for Chapter 13 bankruptcy can still be facing a number of concerns about their case, but all people in this position should know that they are preparing to take a journey that will lead to a much cleaner financial picture. It takes three to five years to complete a Chapter 13 repayment plan, but the rewards are usually worth the effort.

The truth is that there are numerous benefits to filing for Chapter 13 bankruptcy in Arizona. Chapter 13 allows people to correct damaging missed payments and avoid repossessions that can be even worse for their credit records.

Common Advantages of Chapter 13

Chapter 13 is better known as the wage earner’s plan because it allows people with regular incomes to repay all or a portion of their debts. The Chapter 13 repayment plan can offer a number of advantages to people including:

- Consolidate All Your Debt Into a Single Payment — People who file for Chapter 13 rarely pay back all of their debts, and their creditors must accept the Chapter 13 plan that is approved by the court provided it complies with the Bankruptcy Code. The debtor only needs to make one payment a month to their trustee, who then distributes the funds to the creditors.

- Deal with a Trustee — A Chapter 13 trustee generally wants to see a person complete their repayment plan, so they may be willing to work with a person when any issues arise. The trustee can also deal with the creditors.

- Cheaper Than Chapter 7 — Many people filing bankruptcy cannot afford to spend more money, so it is important to note that the filing fees for Chapter 13 are less than Chapter 7.

- Keep Your Home — Unlike Chapter 7 cases in which most people must part with their houses, a person filing for Chapter 13 often has the opportunity to save their home even when it is in foreclosure.

- Cure the Default on Your Mortgage — People who are behind on mortgage payments can work their repayments into their plan to catch up on past due payments.

- Foreclosures Can Be Stopped — A foreclosure may be stopped at any time by filing a bankruptcy petition before the sheriff commences a sale of the property. It is important to take action before the sheriff sells the property.

- Discharge a Second Mortgage — People who more than their homes are worth on their first mortgages may be able to get their second mortgages thrown out.

- Keep Your Car — Even when you are behind on motor vehicle payments, Chapter 13 can allow you to keep your automobile. You will need to file for Chapter 13 before your car is repossessed and sold at auction.

- Pay Fair Market Value for a Car — If you are willing to part with a motor vehicle that you owe more than it is worth, you may be able to pay only for what the car is worth.

- Reduce the Interest Rate on the Car Loan — When you took out a car loan with a high interest rate, Chapter 13 may be able to get the rate reduced to something more reasonable.

- Keep Your Income Tax Refund — Chapter 13 may allow you to ask the court to incorporate your annual income tax refund into your chapter 13 bankruptcy plan, whereas chapter 7 involves people losing some or all of their income tax refund.

- No Penalty or Interest on Non-Dischargeable Tax Debts — A person who owes income taxes for tax years over three years before filing their bankruptcy petition can have those income taxes discharged. Chapter 13 lets people pay non-dischargeable taxes over a period of three to five years without further penalties or interest.

- Right to Convert — While you may file for Chapter 13, you have the right to convert your case to Chapter 7 later.

- Rebuild Your Credit — A Chapter 13 discharge is not as unfavorable as Chapter 7 because a person is generally making an effort to repay a portion of their debt. Many people in Chapter 13 repayment plans can take steps to improve their credit while they are in repayment plans, so credit scores can improve even while a person is still paying.

- Less Credit Report Impact — A Chapter 7 case stays on your credit report for 10 years but Chapter 13 only lasts seven years.

If you are still having doubts about what Chapter 13 could do for you, make sure to take the time to speak to a legal professional who can outline exactly how Chapter 13 could improve your future. Many people understandably have several concerns about filing for Chapter 13, but the truth is that most people find that taking the initial steps proves to be the best thing they could have done to reverse their situations.

Chapter 8 What Is The Downside of Filing For Chapter 13 Bankruptcy in Arizona?

People who are filing for Chapter 13 bankruptcy can easily become wrapped up in some of the many immediate benefits they are likely to see as soon as they file. Just as there are certain to be advantages to filing for Chapter 13, people are also sure to face more than a few drawbacks.

When you file for Chapter 13, you are telling a court you cannot manage your debts and need help repaying them, which is certainly better than just asking the court to cover all of the costs without contributing anything. Even though a person may be willing to repay a portion of their debts in Chapter 13, there is no getting around that any kind of bankruptcy filing generally carries some negative connotations.

Potential Disadvantages of Chapter 13

While Chapter 13 has a number of compelling reasons for people to use it to file for bankruptcy, not all people feel debt relief right away. Many individuals filing for Chapter 13 are still dealing with all kinds of bills that are difficult to catch up on, although Chapter 13 can provide some hope that they will catch up eventually.

Chapter 13 is typically beneficial because a bankruptcy trustee will work with people to help them complete repayment plans, but people can still face all kinds of potential disadvantages to a Chapter 13 case that may include:

- Length of Repayment Plans — You are going to be spending three to five years repaying your debts.

- Disposable Income — Your debt will be paid using your disposable income, meaning that pretty much all money you make over the next three to five years will be committed to your Chapter 13 repayment plan.

- Credit Report — Filing Chapter 13 will remain on a person’s credit report for 10 years.

- No More Credit Cards — A person who files for bankruptcy generally forfeits all their credit cards, although many new credit card offers will begin arriving as soon as a person files for bankruptcy.

- Mortgage Hopes — For people who do not own their own homes, filing for bankruptcy can eliminate all hopes of getting a mortgage.

- No Relief on Domestic Support Obligations — Chapter 13 or any chapter of bankruptcy will do nothing for a person’s requirement to pay child support, spousal support, etc.

- Student Loan Debt Remains — A person cannot discharge student loans in bankruptcy unless they can prove that loan payments impose an “undue hardship” on them, their family, and their dependents.

- Certain Debts Remain — Even after a person completes a Chapter 13 repayment plan, they can still be liable for mortgage liens or other debts.

When you file for Chapter 13, it will lengthen the amount of time you must wait before you can declare bankruptcy again. You will have to wait two years to file for Chapter 13 again after completing a Chapter 13 case, and you have to wait six years before you can file Chapter 7 after filing for Chapter 13.

There also remains the fact that many people who enter Chapter 13 repayment plans simply are not able to complete them. Many of these same individuals did not knowingly refuse to make payments but instead had some kind of unfortunate event arise, such as unemployment, that made it impossible for them to continue making payments.

The problem with not completing your Chapter 13 repayment plan is that failure to complete a plan can mean that a person loses some of their assets. People who have concerns about Chapter 13 plans may be better served by examining their debt management program, debt consolidation, debt settlement, and credit counseling options.

According to the most recent Bankruptcy Abuse Prevention and Consumer Protection Act (BAPCPA) report, 38 percent of the 733,000 bankruptcy petitions filed were Chapter 13 and 37 percent of the 764,000 consumer cases closed that year were Chapter 13. A total of 280,990 chapter 13 consumer cases filed were closed by dismissal or plan completion, and 159,558 of these cases were dismissed with the 43 percent of cases closed being a decrease from the previous year.

The other downside of Chapter 13 for most people is that Chapter 13 will be more expensive to hire an attorney for than Chapter 7. A Chapter 7 case only lasts a couple of months and does not involve as much work, but a lawyer in Chapter 13 cases has a lot more to do.

Chapter 9 Can You File Chapter 13 Bankruptcy in Arizona on Student Loans?

A Chapter 13 petition involves three types of claims: priority, secured, and unsecured. In Chapter 13, student loans are nonpriority unsecured debts, which means they are the same as credit cards and medical bills, and a person is not required to pay them off in full through a Chapter 13 repayment plan but must continue to pay them after a Chapter 13 bankruptcy plan is over.

According to the United States Department of Education Federal Student Aid website, people can get federal student loans discharged in bankruptcy when they file a separate action known as an adversary proceeding. With an adversary proceeding, you have a separate lawsuit within a bankruptcy case that determines the dischargeability of a debt.

Discharging Student Loans in Chapter 13

Can a debtor maintain a minimal standard of living for themselves and their family if forced to repay their loans?

Is a debtor’s current financial situation unlikely to change during their repayment period?

Has a debtor tried to get out of paying their student loans, and can they demonstrate they made a good-faith effort to repay them?

It can be wise to examine the rates of success others have had with discharging student loans in bankruptcy, and an American Bankruptcy Law Journal study found that only 0.1 percent of student loan debtors filing for bankruptcy even tried to discharge their student loans. An estimated 40 percent of people who initiated adversary proceedings discharged all or a part of their student loan debts.

Here are some recent court decisions relating to student loan debt in bankruptcy cases:

- The United States Bankruptcy Court for the District of Arizona ruled in Edwards v. Educ. Credit Mgmt. Corp. (In re Edwards), Case No: 3:14-bk-16806-PS (Bankr. D. Ariz. Mar. 31, 2016) that a debtor satisfied her burden of proof on each of the three Brunner tests and concluded that a partial discharge was not appropriate because the debtor did not have the capacity to repay any portion of her student loans, so it wholly discharged the student loans at issue under 11 U.S Code § 523(a)(8).

- In a January 2014 case, the United States Bankruptcy Court for the District of Arizona found a debtor’s loans to be dischargeable under the Brunner test.

- Another adversary proceeding in July 2013 involved a debtor representing themselves and got the United States Bankruptcy Court for the District of Arizona to rule that their student loan debt would be discharged in its entirety.

- The United States Bankruptcy Court for the District of Arizona ruled in Greenwood v. Educ. Credit Mgmt., 349 B.R. 795 (Bankr.Ariz. 2006), that a debtor satisfied all three prongs of the Brunner test and a judgment would be entered in their favor on the complaint, which stated that the debtor was entitled to a discharge of his student loan obligations which exceeded $39,000.

The “Brunner test” is the common phrase in many these decisions, and most states use the Brunner test to determine undue hardship claims. The Brunner test is a three-pronged test simply asking the following:

- Can a debtor maintain a minimal standard of living for themselves and their family if forced to repay their loans?

- Is a debtor’s current financial situation unlikely to change during their repayment period?

- Has a debtor tried to get out of paying their student loans, and can they demonstrate they made a good-faith effort to repay them?

People will be more likely to pass the Brunner test if they are older, are likely not to make too much money for the remainder of their lives, and have tried to pay off their loans. The test is most often applied during an adversary proceeding, which begins when a complaint is filed asking the court to rule on an issue relating to a bankruptcy case.

An adversary proceeding is given a new case number separate from the number of the associated bankruptcy case and will be governed by Part VII of the Federal Rules of Bankruptcy Procedure (FRBP). Several actions can be brought by an adversary proceeding, but you will want your cause to be a Proceeding to determine the dischargeability of a particular debt under § 523.

Discharging student loan debt is challenging but not altogether impossible in Arizona, so you will need to make sure you are working with a skilled lawyer. You are going to want to be sure you have legal representation so you can have a full understanding about what kinds of student loan debt you may be able to get discharged or find other solutions that can make your life easier.

Chapter 10 How Long After Chapter 13 Bankruptcy in Arizona Can You Buy a House?

Several people who file for Chapter 13 bankruptcy wonder how long it will be before they can buy a home, and the good news is that Chapter 13 can be easier to work with in this regard than Chapter 7. In most cases, people can apply for mortgages as soon as one year after filing for Chapter 13.

Only certain types of loans will be available within one year of filing, however, as most conventional loans will require a person to wait at least two years. Whether your case is dismissed as opposed to discharged can also be an important consideration as bankruptcy dismissals will mean a person must wait four years.

Mortgage Options after Bankruptcy

Federal Housing Administration (FHA)

United States Department of Agriculture (USDA)

Department of Veterans Affairs (VA)

If a person is hoping to get a mortgage in Arizona, they will need to know their different mortgage options and how bankruptcy could affect them. Most conventional mortgage lenders such as Fannie Mae and Freddie Mac stipulate that a person cannot obtain a mortgage until four years after bankruptcy discharge or dismissal.

Conventional mortgages are again more difficult to qualify for after Chapter 13, but government-backed mortgages insured by one of three federal government agencies can be a much more preferable option. The federal agencies include:

- Federal Housing Administration (FHA) — According to the United States Department of Housing and Urban Development (HUD), FHA loans have been helping people become homeowners since 1934. Individuals must satisfy certain minimums for an FHA home loan, including having a credit score of at least 580, having not filed for Chapter 7 bankruptcy in the last two years, showing proof of income, affording a down payment, and a home being purchased being a primary residence. The FHA does not make loans but instead insures loans made by private lenders, so a person will have to seek out an FHA-approved lender. They then need to apply or get pre-approved for an FHA loan, and buying a home involves an FHA property inspection and appraisal, FHA underwriting and approval, and then paying closing costs and fees.

- United States Department of Agriculture (USDA) — The USDA loan program helps low- and middle-income consumers become homeowners by allowing them to purchase homes with $0 down while receiving competitive interest rates and low mortgage insurance costs. Getting prequalified with a USDA lender involves a credit check and a brief income review, as USDA determines applicants using income from every adult earner in a household. A person will want to know how much they need to borrow and their household’s total monthly income before they apply. A person will need to find a USDA lender, and additional USDA requirements will include property needing to be a person’s primary residence, household income satisfying USDA income limits, a buyer being a United States citizen, property being in a USDA-eligible location, and a buyer having a minimum 640 FICO score. Once a person is preapproved for a USDA home loan, they find a home in a USDA-eligible area and make an offer. USDA home loans go through two stages of loan approval, as all parts of a loan have to be cleared through underwriting first before USDA. A person’s lender and/or USDA can request additional documents or information before approval can be issued. The appraisal is a required step for final loan approval to assess property value, and a satisfactory appraisal will confirm the property values supports the purchase price. Closing occurs within a few days of final USDA approval.

- Department of Veterans Affairs (VA) — A person begins the VA loan process by finding a VA-approved lender. They will have to request a VA home loan Certificate of Eligibility (COE), which requires different documentation depending on their status. A person may want to try to pre-qualify for a loan before they begin home shopping, but they could also go house hunting and sign a purchase agreement. The lender will process an application and order a VA appraisal. When everything is approved, a person simply signs their final papers.

Immediately after filing for Chapter 13, a person needs to take steps to try and restore their credit rating. Several people are reluctant to take out credit cards, but it can be beneficial to maintain a couple of credit cards to use and pay off every month so there is no recurring balance.

Chapter 11 Can I Keep My Car If I File Chapter 13 Bankruptcy in Arizona?

Concerns about the ability to keep a motor vehicle are one of the most common reasons many people choose not to file bankruptcy, but people need to understand that Chapter 13 is much different than Chapter 7 in this respect. Whereas most people filing Chapter 7 are seeking a liquidation of their assets to discharge their debts, people entering Chapter 13 are agreeing to repayment plans.

In turn, people who have already paid for their vehicles can keep the cars so long as creditors are getting enough non-exempt assets that would have been liquidated in a Chapter 7 case. When a person still owes money on their car, they can work the payments on the vehicle into their repayment plan.

Understanding Exemptions in Arizona

Federal bankruptcy laws allow debtors to exempt some of their property under either federal law or the laws of their home state. Motor vehicles are assets listed on Schedule A/B of bankruptcy forms, and the list of exemptions from the United States Bankruptcy Court for the District of Arizona establishes that an exemption of equity in one car not greater than $6,000.

If a debtor or their dependent is physically disabled, the fair market value of a motor vehicle cannot be more than $12,000. Equity is the fair market value of a motor vehicle minus debt to any secured creditor.

A person without an automobile loan who owns their car outright has the same amount of equity as a car’s value. A person who still has a loan determines their equity by subtracting the remaining loan amount from the actual value of the vehicle, so a person who owes $10,000 on an $30,000 car has $20,000 in equity.

A motor vehicle in Arizona is exempt from bankruptcy proceedings if the equity is less than $6,000, and a person is filing on their own. In other words, driving a car that currently has a value of $10,000 but you still owe $5,000 on means that you have $5,000 in equity and you can keep the car.

When a car has more equity than the exemption, a trustee can seize the vehicle and sell it to satisfy a person’s debts. A trustee does not automatically decide to seize all vehicles with more equity than the exemption though, as some cases may require more effort to sell and not be worth the trustee’s time.

Any car can be considered to be a secured debt, meaning a person cannot discharge their car loan in bankruptcy. The only option people have when they are filing bankruptcy and cannot afford to continue to make car payments is to allow the lender to repossess the vehicle.

Some people may also be leasing their motor vehicles, and a car lease is a contract that will not be considered a debt when you file for Chapter 13. A person can continue to lease their car in a Chapter 13 case so long as they remain current on their payments.

If the value of your vehicle is too low, a person can increase their number by using a wildcard exemption. Arizona does not have a wildcard exemption, but federal law allows an exemption of $1,475 plus up to $13,950 of any unused amount of the homestead exemption (or a total of $15,425).

Another possible option in some cases can be redemption, under which a person keeps their vehicle by paying the fair market value of the vehicle in full. It is most useful for people who are upside down on vehicles, and some companies offer redemption loans that can be repaid like ordinary car loans.

The obvious drawback to a redemption agreement for a person filing Chapter 13 is needing to accumulate enough money to pay for the car in one fell swoop, but redemption funding providers are common, and people need to exercise severe caution in dealing with these companies. Many providers charge very high interest rates.

In the end, the three options with a car in bankruptcy will be to reaffirm, in which a person and their lender sign a reaffirmation agreement stating they will continue to make car payments, surrender, in which a person gives up the vehicle, or redemption, in which a person pays based on the car’s value.

Chapter 12 How Long Does Chapter 13 Bankruptcy Stay on Your Credit in Arizona?

The good news for most people filing Chapter 13 bankruptcy is that Chapter 13 will actually do less damage to a person’s credit than Chapter 7 because Chapter 7 cases stay on people’s records for 10 years while Chapter 13 only lasts seven. When the seven years are up, a person does not need to take any action to get the bankruptcy removed from their credit report as the information will be removed automatically.

People need to develop a plan to rebuild their credit immediately after filing for bankruptcy and stick with the plan to improve their credit scores. You will want to be working with an Arizona bankruptcy lawyer who can walk you through the entire process of filing for Chapter 13 and help you determine the steps to take afterward.

How Bankruptcy Appears on Credit Reports

When you file for Chapter 13 bankruptcy, your debts will no longer be unpaid or past due, as they should be reported as discharged. People will have to stay up to date on their credit reports to know what information is being reported.

People will generally begin getting new offers for credit as soon as they file for Chapter 13, and you should be skeptical of many credit card offers that involve high interest rates. There can be good secured credit cards that can be advantageous to sign up for, however.

Some of the best steps a person can take to rebuild their credit rating will include:

- Reviewing Credit Reports — Any person who has filed for Chapter 13 bankruptcy should review all of their credit reports from all three major credit bureaus, Experian, Equifax, and Transunion. Credit reports will allow you to verify that your debts have actually been discharged and are carrying a zero balance. You also want to know every account listed actually belongs to you and is displaying the correct current payment status or open and closed dates. Know what to do if you need to dispute an error by any credit bureau, possibly sending a dispute letter by mail, filing an online dispute, or contacting the agency by phone.

- Make Every Payment — No factor will be as important to a credit rating as payment history, as it accounts for 35 percent of a person’s FICO credit score (30 percent is amount owed, 15 percent is the length of the credit history, 10 percent is credit mix, and 10 percent is new credit). Paying outstanding debts on time improves a credit score but making late payments or defaulting on a loan can hurt a credit score.

- Maintain Low Credit Utilization Ratio — The credit utilization ratio is the sum of all a person’s balances divided by the sum of the cards’ credit limits. A person with $100,000 in credit who uses $25,000 of it has a credit utilization ratio of 25 percent. People should try to keep their credit utilization ratios at less than 30 percent, and they can rebuild their credit faster by keeping as close to 0 percent as possible.

- Apply for a Secured Credit Card — People will get many credit card offers after filing for Chapter 13 bankruptcy. While they are not likely to get traditional credit cards, they could qualify for a secured credit card that is a credit card requiring a security deposit and establishes a credit limit. A person can use a secured credit card just like a traditional credit card in most cases, and people will want to pay their balances immediately at the end of every month to help improve their credit because the secured credit card company will report their payments to the three credit bureaus.

- Seek Authorized User Status — If a person is simply not comfortable with the idea of taking out their own credit cards after filing for Chapter 13, they could have the option of asking a friend or family member if they are willing to add them as an authorized user on one of their cards. So long as the person they are asking has a responsible payment history, being an authorized user can also lead to an increase in credit ratings.

CNBC reported that a Debt.org article showed people with average scores of 680 lose between 130 and 150 points in bankruptcy while above-average scores of 780 can lose between 200 and 240 points. That said, people with scores in the 400s or 500s could actually experience a boost from a bankruptcy filing of as much as 50 points after filing for bankruptcy.